NC1 - Indonesia orders 71% cut in nickel production from the world’s biggest nickel mine

Indonesia just ordered the world’s biggest nickel mine to cut its production quota by 71%.

And the nickel price started running immediately after the news…

Our Investment Nico Resources (ASX: NC1) is already up 12% off the back of that news…

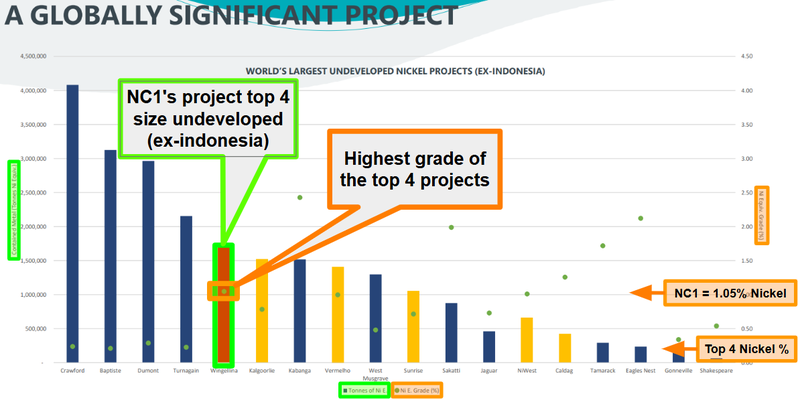

NC1 owns a giant 187.3Mt nickel-cobalt resource in outback Australia and the project has an estimated 1.698Mt of nickel and 106kt of cobalt.

NC1’s project is actually one of the top 4 largest undeveloped nickel projects in the world - and of the top 4 it has the highest grades:

(source)

When we added NC1 to our portfolio in January this year, we did so because we thought that there are factors on both the supply and demand side for nickel brewing.

We think that the demand side is being understated due to the large influx of robots that we are now seeing begin to hit the market.

Especially humanoid robots that have started to get some mainstream attention.

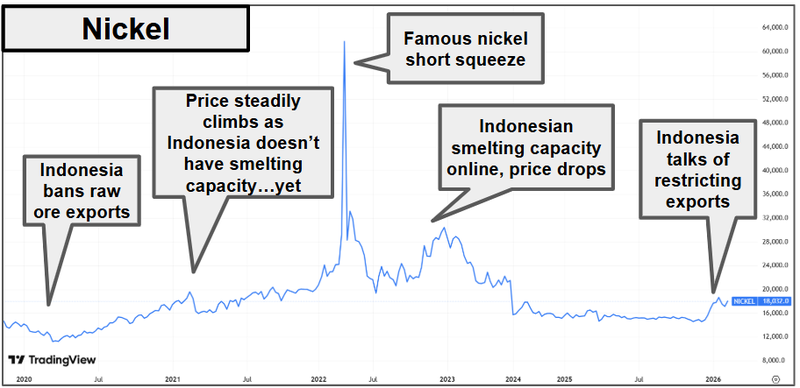

On the supply side, a few years ago now Indonesia began to flood the nickel market with supply from new mines which dropped and suppressed the price.

Indonesia produces ~65% of the world’s nickel and has flooded the market with supply - causing prices to trade at relatively low levels to long run averages.

But recently, market wide fears of restrictions on production out of Indonesia have put a bid under the nickel price - nickel is up ~20% inside the last 6 months, back to ~US$18,000 overnight.

(source)

There have been rumblings coming out of Indonesia the past couple of months that they have been looking to restrict supply (at least partly due to the current low prices).

Which has led to the price jumping more than a bit over the past 2-3 months..

We covered these early rumblings in our initiation note, specifically in this section: We think it’s time to go long nickel…

Here are some of those recent headlines we included in that:

In that section we specifically said “All it takes in today’s less globalised version of the world for a few export bans or countries to threaten export controls and we could be looking at a completely different nickel industry.”

Last night it appears to be playing out as we are hoping on the back of the news.

Nico Resources

ASX: NC1

Back in late 2022, NC1 released a Pre Feasibility Study (PFS) which showed a NPV at the time of A$3.34BN using a base case sale price of US$21,472/t nickel.

It also included a NPV of A$6.54BN at a price of US$30,000/t nickel… So NC1 is highly leveraged to the nickel price, which is part of the reason we made our Investment here.

While we aren’t yet at the base case price, it has now gotten much closer at ~US$18,000/t, up significantly on the lows of near ~US$14,000/t in early April and mid December last year.

In mid January it was as high as ~US18,750, so should similar updates continue to come out of Indonesia, there is potential for the nickel price to continue to rise on concerns of a lack of supply.

We need to point out that NC1's PFS is from late 2022, so the costs associated with this NPV are over 3 years old so should be read with caution, although an update to this, a DFS (Definitive Feasibility Study) is on the way.

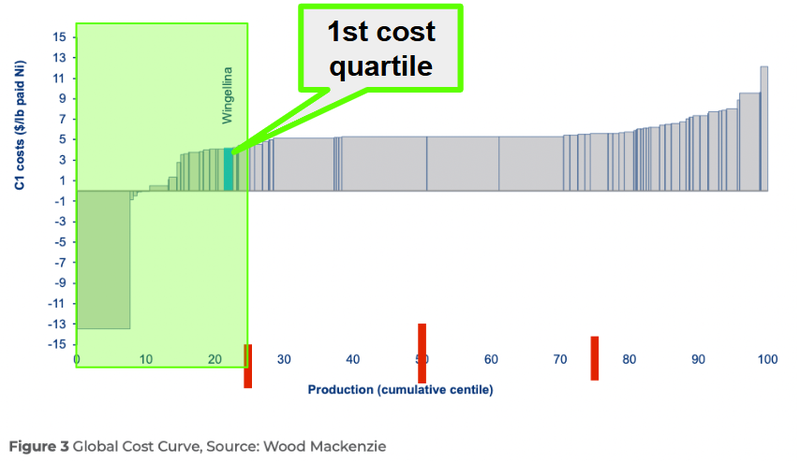

The prior PFS showed that NC1’s project was not only large scale, but in the first cost quartile (which is where you want to be generally to survive market slowdowns).

(source)

The 9 Reasons We Invested in NC1

- NC1 has one of the biggest undeveloped nickel-cobalt projects in the world

- Current market cap is only ~$41M.

- We are backing mining legend Peter Cook (“Cookie”) here.

- Lowest cost quartile once in production

- We think future demand for nickel will be underwritten by a mega thematic (humanoid AI robots)

- We think NC1 is the most leveraged nickel exposure on the ASX (basically a giant call option on nickel prices)

- Project is advanced with a PFS completed in 2022 and a DFS on the way

- Spin out from ~$1BN tin miner Metals X

- Tight and clean capital structure

Check out our full initial article here: Our Latest Investment: Nico Resources (ASX: NC1)

What do we want to see NC1 do next?

Objective 1: Drill out and upgrade defined resources

We want to see NC1 drill out and upgrade its current resources. We are especially looking for increases to the categories of the resources.

Milestones:

🔲 Drilling commences

🔲 Drilling completed

🔲 Resource upgrade completed

Objective 2: Definitive Feasibility Study (DFS)

We want to see NC1 deliver its DFS - and hopefully improve on the numbers released in the PFS in 2022.

Milestones:

🔲 Processing flowsheet optimisation

🔲 Mine plan/infrastructure optimisation

🔲 Definitive Feasibility Study completed

Objective 3: Project funding solution

Ultimately we want to see NC1 reach FID and finance the build of its project.

Between now and then a cornerstone coming in and backing the company could de-risk financing materially (similar to what we saw happen with our Investment Canyon Resources and Eagle Eye Asset Management).

Milestones:

🔲 Final Investment Decision

🔲 Project Debt

🔲 Project Equity

🔲 Strategic partner comes into NC1 or NC1’s project